Managing your salary wisely can feel overwhelming, especially when monthly expenses keep rising. Whether you’re earning ₹30,000 or ₹1,00,000 a month, the secret isn’t in earning more — it’s in budgeting smarter.

Enter the 50-30-20 rule — a simple yet powerful method to plan your income without spreadsheets or stress. In this guide, we’ll explain how this rule works, adapt it to Indian salaries, and give you real examples to start using it today.

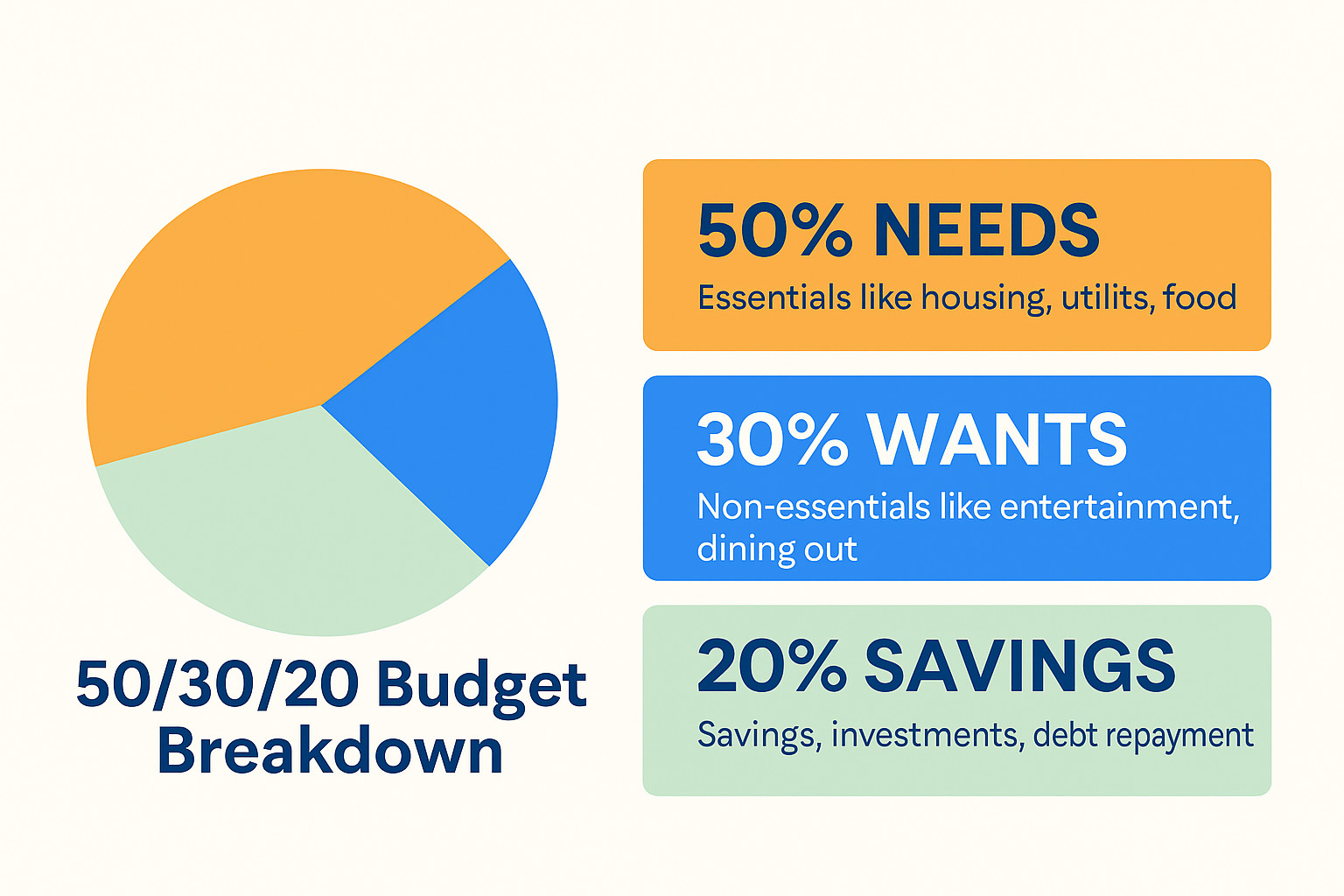

✅ What is the 50-30-20 Rule?

The 50-30-20 rule is a money management strategy that divides your monthly income into three clear buckets:

- 50% – Needs: Rent, groceries, utility bills, transport, education, EMIs

- 30% – Wants: Eating out, subscriptions, entertainment, shopping

- 20% – Savings: Investments, emergency fund, retirement planning

This approach keeps your lifestyle in balance while ensuring you’re saving for your future. It’s perfect for salaried people who want a simple yet effective structure for their income.

📊 Example 1: ₹30,000 Monthly Salary

| Category | Amount (₹) |

|---|---|

| Needs (50%) | ₹15,000 |

| Wants (30%) | ₹9,000 |

| Savings (20%) | ₹6,000 |

Suggested breakdown:

- ₹3,000 – Mutual fund SIP

- ₹2,000 – Emergency fund (liquid FD or RD)

- ₹1,000 – Short-term goal (vacation, gadget)

📊 Example 2: ₹50,000 Monthly Salary

| Category | Amount (₹) |

|---|---|

| Needs | ₹25,000 |

| Wants | ₹15,000 |

| Savings | ₹10,000 |

Suggested savings plan:

- ₹5,000 – Equity mutual fund (Flexi cap or Index)

- ₹3,000 – NPS (for retirement + tax saving)

- ₹2,000 – Digital gold or short-term FD

📊 Example 3: ₹70,000 Monthly Salary

| Category | Amount (₹) |

|---|---|

| Needs | ₹35,000 |

| Wants | ₹21,000 |

| Savings | ₹14,000 |

Advanced savings idea: Split the ₹14K into SIP, ELSS (for 80C), and travel goal fund. Diversify based on risk tolerance.

💡 How to Automate the 50-30-20 Rule

Here’s how to make this system work without daily tracking:

- Auto-debit SIPs: Set them for the 1st of every month

- Use 3 accounts: Salary, Bills, and Savings (auto-transfer to each)

- Track via apps: Walnut, Money Manager, or INDmoney

- Cash-based “Wants”: Withdraw fun money in cash to avoid overspending

🚫 Common Mistakes to Avoid

- Putting savings last: Always “pay yourself first” — automate it

- Confusing needs and wants: Upgrade phone ≠ need

- No budget review: Recheck your percentages every 3–6 months

- Overspending via credit card: It distorts category limits if you don’t track payments

📥 Free Salary Split Calculator (Download)

Use our Excel calculator to instantly calculate 50-30-20 breakdown for your income from ₹30K to ₹1L in ₹10K steps.

🎁 Download Our Free 50-30-20 Salary Planner

Instantly calculate your ideal Needs, Wants & Savings split from ₹30K to ₹1L. Simple Excel format with built-in formulas!

💬 Frequently Asked Questions

❓ Is this rule practical in metro cities like Mumbai or Bengaluru?

Yes, but rent may consume more than 50%. In such cases, reduce “Wants” to 20% and stay consistent with 20% savings.

❓ What if my income is irregular?

Apply the 50-30-20 rule to your average monthly income. Save more during high-income months.

❓ Can I switch to 70-20-10 or 60-30-10?

Yes. The idea is to build a system. Modify percentages to match your goals — just keep savings a non-negotiable.

🎯 Final Thoughts

The 50-30-20 rule is more than a budgeting trick — it’s a mindset. When followed consistently, it helps you reduce money stress, control spending, and steadily grow wealth.

Try it for 1 month. Track your expenses. Stick to the limits. Watch how you feel more confident with money — without compromising your lifestyle.

💬 Let us know in the comments: What’s your monthly income — and how close are you to a 50-30-20 split?